Low inventory 🏠 and the crash that hasn't come

Low inventory 🏠 and the crash that hasn't come

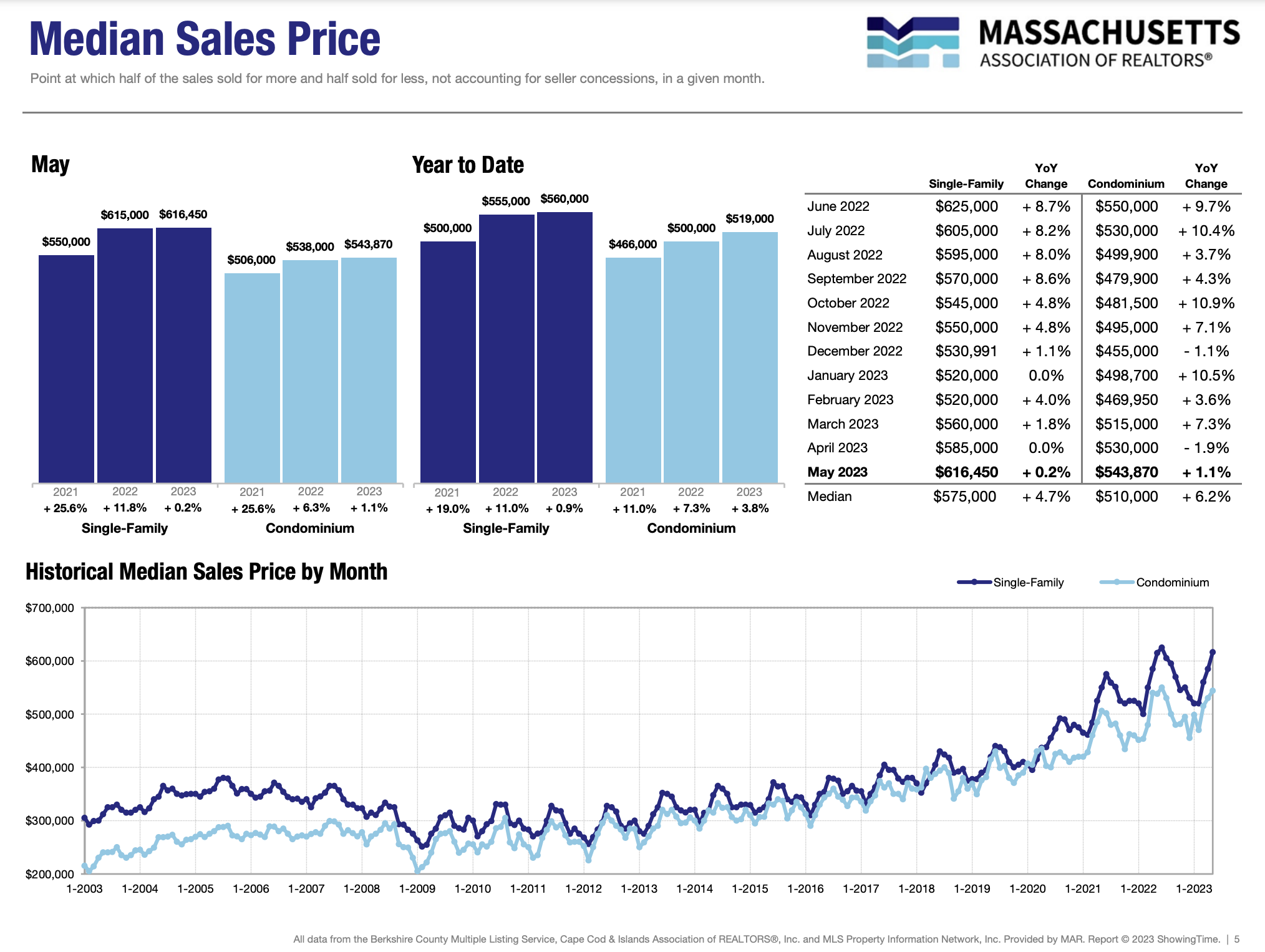

Despite the Fed’s best efforts, prices have been remarkably sticky

For the first half of 2023, one of the biggest challenges facing buyers has been “low inventory” - that is, vanishingly few homes for sale. Home buying is a unique process in that a buyer is choosing only from currently available houses, and not from every property that might possibly meet their needs. In New England in particular, where new construction faces very limited available land and high building costs, this means that if sellers don’t want to sell, there just aren’t homes available. For buyers not willing to settle merely for a rental replacement, demand is still exceedingly high and competition fierce, in addition to the higher interest rates.

Low inventory is not all good news for sellers: even with buyer demand higher than inventory, a dearth of close comps (comparable recent sales) means appraisers are working with limited data and appraisals are sometimes coming in low - leading to price negotiations in some cases, even after a bidding war.

Not all sellers are seeing multiple offers, either, despite the extremely short inventory. Buyers are being more selective: they’re not prepared to make a move and lock in a rate for something that won’t be a fit for their family longer term. “Starter” homes and condos are taking a hit as a result; off-street parking is more important than ever, and room to grow into a home is often a priority. As a result, unlike recent years, if you see something that’s been sitting on the market, it might not be due to a major flaw - possibly just a minor quirk. Check it out, because there could be room to negotiate.

Home price appreciation is not a straight line: there are seasonal variations even in a normal year. A low appraisal now reflects the slow market of the past 2-6 months, but it doesn’t mean the property isn’t “worth it” and might not appraise at our above offer price by the fall. Trust your numbers, above all: are you comfortable at that price and monthly payment for the long haul?

But why might sellers choose to wait? What’s fueling low inventory this in so many markets? A client asked me this last week, and the short answer is: it’s complicated.

Most sellers have realized they can’t be certain of achieving the premium sale prices of 2021 and 2022 with interest rates making up a higher portion of buyers’ monthly payments - this is what we mean when we say “purchasing power” has been reduced by rising rates. The vast majority of buyers make decisions based on their total monthly payment (principal, interest, taxes, and insurance - PITI), not on purchase price - and this means that elevated interest rates impact price for everyone but cash buyers.

Some sellers also might not have their next property secured. If they have a low interest rate on their current house, especially from 2018-2021, they may not be prepared to give that up. Renovations and additions are more appealing to sellers looking for more space, if their interest rate is currently locked at an historic low. This type of prospective seller may make improvements instead of relocating, or may hold out to see if rates come down again in the next year or two.

Buyers, remember that not all sellers have to sell - don’t wait for the price to be lowered to you. If there’s a number where something works for you, write it up! A seller could change their mind and rent or stay if they’re not getting offers, so it behooves you to express interest.

Sellers, remember that - though multiple offers as a norm have been nice - it’s much more stable and historically normal for things to move a bit slower. It only takes one! Take care of the little things, and otherwise, price well for your goals.

Stay cool,

Kate